Florida is the third-largest solar market in the United States — behind only California and Texas — and also one of the most complicated states to navigate as a solar buyer in 2025.

The sun is excellent. The incentives are real. The electricity rates from FPL and Duke Energy have been climbing steadily for four years. On paper, Florida looks like one of the strongest solar arguments in the country. Then you call your homeowner’s insurance company about adding panels, and the conversation gets complicated fast.

This post covers what actually makes Florida solar different from every other state — the good numbers and the problems that don’t show up in most installer pitches.

The Florida Solar Advantage: Why the Numbers Start Strong

Florida averages 2,900–3,100 peak sun hours per year across most of the peninsula — among the highest in the continental US, second only to the desert Southwest. Phoenix gets more sun than Miami, but not by much, and Miami has far higher electricity rates.

Florida Power & Light (FPL), which serves roughly half the state’s population, has raised residential rates multiple times since 2021. Duke Energy Florida and Tampa Electric have followed. As of 2025, average residential rates in most Florida territories run $0.13–$0.16/kWh — meaningfully above the national average of $0.12/kWh and rising.

For a Florida homeowner using 1,500 kWh/month (typical for a 2,000 sq ft home with central AC running hard through the summer), annual electricity costs run $2,340–$2,880. That’s the baseline the solar savings work against — and it’s a strong number.

Add the federal 30% IRA tax credit, and the effective cost of an average Florida solar install (8–10kW, roughly $26,000–$32,000 gross) comes down to $18,200–$22,400. At Florida’s rates and sun hours, payback periods run 6–9 years for most well-designed systems — competitive with any market in the country.

Florida’s Two Incentives Most Homeowners Miss

The sales tax exemption. Florida charges no sales tax on the purchase of solar energy systems. At Florida’s 6% sales tax rate, this saves $1,560–$1,920 on a typical system. It applies to panels, inverters, and racking — everything directly part of the solar system. It doesn’t apply to installation labor, but the equipment exemption alone is meaningful. This exemption doesn’t show up in most installer quotes as a line item because it’s baked in — you just don’t pay it. Worth confirming explicitly that your quote reflects this.

The property tax exemption. Similar to Texas, Florida exempts the assessed value added by a solar installation from property taxes — 100% of the added value, indefinitely. On a home in a county with a 1.5% property tax rate, a solar system that adds $20,000 to assessed value saves $300/year in avoided property taxes. Over 25 years, that’s $7,500 — real money that most payback calculations ignore entirely.

Neither of these requires an application. They’re automatic for any qualifying solar installation by a licensed contractor. DSIRE’s Florida incentives database lists both with the current statutory citations if you want to verify before signing anything.

Florida Net Metering: Still Good, But Under Pressure

Florida currently has statewide net metering at or near full retail rate — one of the more homeowner-friendly net metering policies in the Southeast. If your panels produce more than you use in a given month, the excess flows to the grid and you receive a credit at your utility’s retail rate, carried forward to offset future bills.

This is significantly better than what most of the Southeast offers and better than California’s new NEM 3.0 export rates. It’s one reason Florida solar math has held up well even as California’s got more complicated.

The concern: Florida utilities — particularly FPL — have lobbied repeatedly for reduced net metering compensation. The Florida Public Service Commission has so far maintained retail-rate net metering, but the regulatory environment has been contentious. This is not a reason to avoid solar in Florida, but it’s a reason to understand your interconnection agreement and to size your system to your actual usage rather than oversizing in expectation of banking large credits.

Marcus — who has contacts at installers working both Texas and Florida markets — told me the same thing he says about every market with net metering risk: “Don’t design a system that depends on selling power at a favorable rate for its payback math. Design it to cover your consumption.”

That’s good advice everywhere. In Florida in 2025, it’s particularly relevant.

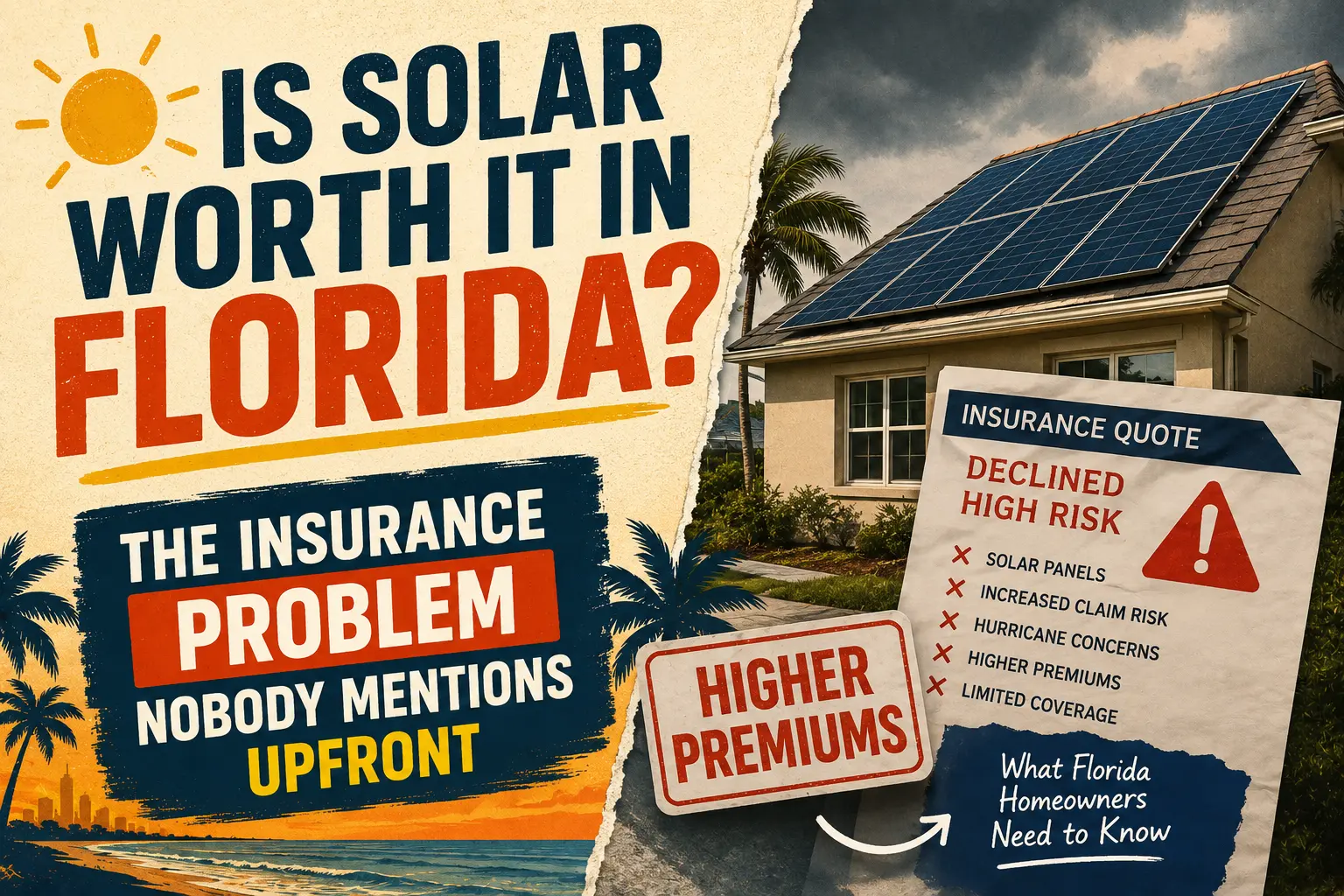

The Insurance Problem (And Why It’s Florida-Specific)

Here’s the part most solar salespeople in Florida don’t bring up until after you’ve signed.

Florida has the most distressed homeowner’s insurance market in the country. Dozens of insurers have exited the state since 2021. Citizens Insurance — the state-backed insurer of last resort — now covers nearly 20% of Florida homeowners. Premiums have doubled or tripled in many counties.

Adding solar panels to this situation creates a specific complication: many Florida insurers will not cover solar panels under a standard homeowner’s policy, or will require a separate rider at additional premium. Some will not renew your policy at all if you add panels without prior notification. A few have canceled policies retroactively when solar was discovered on a roof.

The coverage gap issue matters because solar panels are not cheap to replace. A hailstorm or hurricane that damages your panels — not rare in Florida — needs to be covered by something. If your insurer excludes panels, you’re exposed.

What to do before you sign a solar contract in Florida:

- Call your current insurer first. Ask explicitly: “If I install rooftop solar panels, will they be covered under my current policy? Will my premium change? Do I need a rider?” Get the answer in writing.

- If coverage is denied or a rider is required, get quotes from other insurers before signing the solar contract. Your insurance situation may affect your total cost calculation significantly.

- Ask your installer for documentation of the panel wind rating. Florida Building Code requires panels to meet specific wind uplift ratings — 140+ mph in most counties, 175+ mph in Miami-Dade and Broward under the High-Velocity Hurricane Zone standards. Installers who are not familiar with Florida building code compliance by county are not the right installer for a Florida home.

The insurance issue doesn’t make Florida solar not worth it. It makes it a more complex purchase than in most other states. Going in aware of it puts you in a far better position than discovering it post-install.

Hurricane Resilience: The Paradox

Here’s the thing about Florida solar and hurricanes that most people get wrong in both directions.

The wrong assumption: “Solar panels will help me during a hurricane.” They won’t — at least not without a battery. Standard grid-tied solar systems automatically shut down during a grid outage. This is a safety requirement (to protect utility workers from backfed power). If you want your solar system to keep running during a storm outage, you need battery storage with a backup gateway that can island your home from the grid.

The other wrong assumption: “Hurricanes will destroy my panels.” Modern solar panels rated to Florida’s wind requirements have an excellent hurricane track record. After Hurricane Ian in 2022, post-storm assessments found that properly permitted and installed solar systems in the impact zone had a very low failure rate — the limiting factor was almost always roof damage, not panel damage. A solar system on a roof that doesn’t survive a hurricane was a roof problem, not a solar problem.

The practical upshot: if hurricane resilience is part of your reason for going solar in Florida — which is a reasonable motivation given the grid outage reality after major storms — you need a battery paired with the system. Battery without solar is expensive insurance. Solar with battery in Florida is genuinely useful backup that also generates daily savings. The combination makes more sense in Florida than almost anywhere else in the country, for similar reasons to why California homeowners need battery storage under NEM 3.0 — though the reasoning is different.

Florida by Utility: What to Know Before You Quote

Florida Power & Light (FPL): Largest utility, serves Southeast and East Coast Florida. Net metering at retail rate. Strong solar market, many competing installers. FPL also has its own solar subscription program (FPL SolarTogether) — a community solar option that doesn’t require rooftop installation. Worth comparing if your roof isn’t ideal.

Duke Energy Florida: Serves Central Florida including Tampa Bay, Citrus County, and parts of the Panhandle. Net metering in place. Permitting timelines in Duke territory have historically been longer than FPL — plan for an additional 3–6 weeks on the interconnection process.

Tampa Electric (TECO): Serves Hillsborough County. Net metering policy similar to Duke. Good solar market with active local installer competition.

JEA (Jacksonville): Municipal utility — different regulatory structure. Has its own solar interconnection rules that differ from investor-owned utilities. Worth reading JEA’s specific interconnection requirements before getting quotes from installers who may not be familiar with them.

For current net metering rates and interconnection requirements by utility, SEIA’s Florida market data is updated regularly and covers policy developments that installer websites typically don’t.

My Florida Assessment

Strong solar case, with homework required on insurance and wind ratings that most other states don’t demand.

The sun, the rates, the two hidden incentives (sales tax exemption and property tax exemption), and the still-functional net metering policy all point toward yes. The insurance market complication and the hurricane building code requirements add pre-signing steps that Texas and most other states don’t have.

Florida homeowners who do that homework — call the insurer before signing, confirm the installer knows Florida building code by county, size the system to consumption rather than to a favorable net metering rate that might not last — end up with solar systems that perform well and economics that make sense.

The ones who skip those steps are the ones with surprises in year two.

Start with your insurer. Then get quotes. In that order.

— Allen