$8,463. That’s the check — technically a tax credit, which is better than a check — that I received from the federal government the spring after my solar system went live.

My system cost $28,210 installed. Thirty percent of $28,210 is $8,463. The math is that simple. The details — what’s included in that 30%, who can actually use it, what happens if you can’t use it all in one year, and how to actually file for it — are where things get worth explaining carefully.

This is the most valuable financial incentive in residential solar, and it’s one of the most misunderstood. Here’s everything you need to know before you file.

What the Credit Actually Is

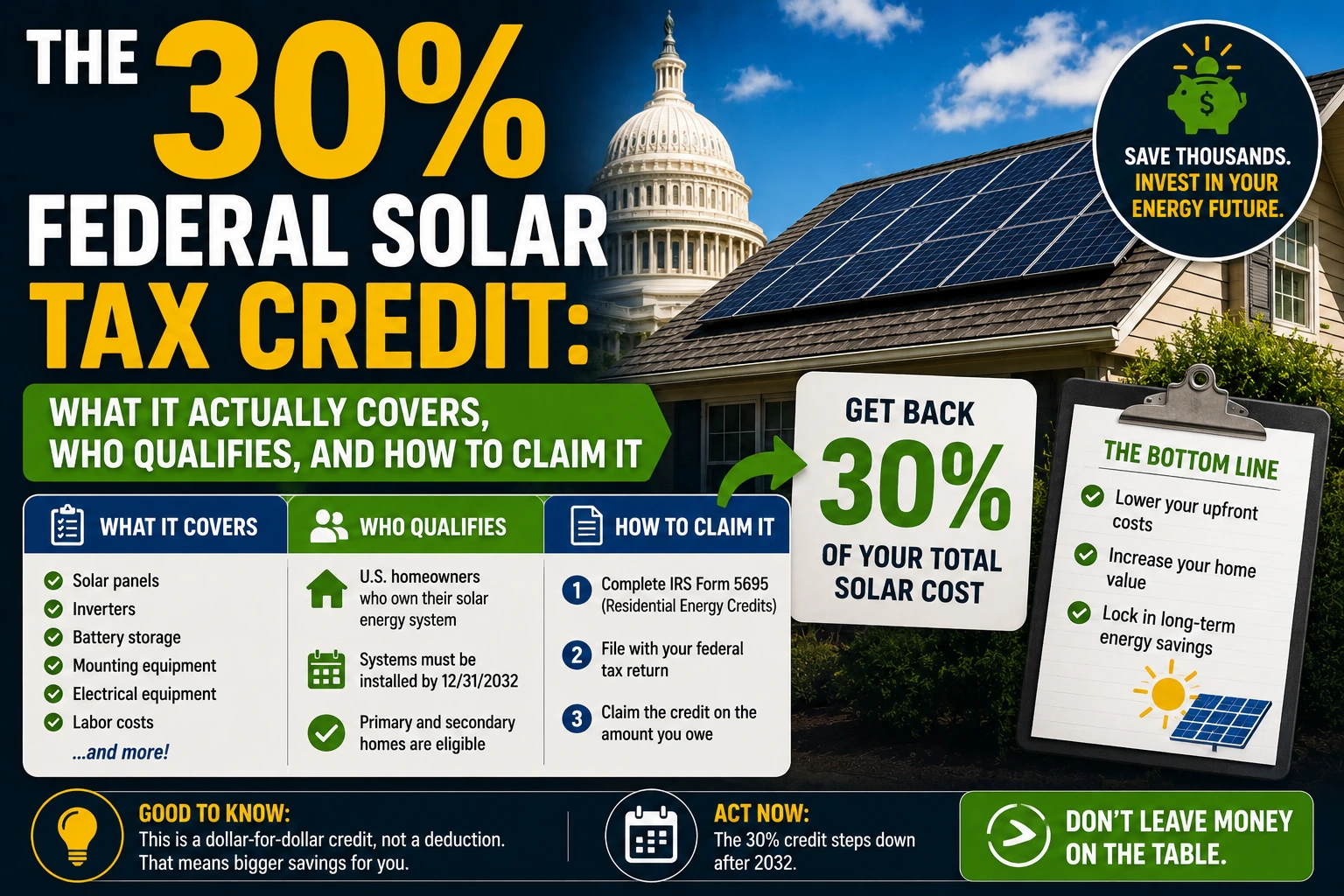

The federal solar tax credit — formally called the Residential Clean Energy Credit — is a dollar-for-dollar reduction in the federal income taxes you owe. It is not a rebate, not a deduction, and not a check the government sends you. It reduces your tax liability.

The distinction matters. A tax deduction reduces your taxable income, saving you money at your marginal tax rate (20–37% for most homeowners). A tax credit reduces your actual tax bill by the full credit amount. A $8,463 tax credit saves you $8,463 in taxes — regardless of your bracket.

The current credit rate: 30% of the gross qualified cost of your solar installation. This rate applies to systems placed in service from 2022 through 2032. Under the Inflation Reduction Act, it then steps down to 26% in 2033 and 22% in 2034 before expiring for residential installations at the end of 2034 — unless Congress extends it again, which it has done before.

The practical implication: if you’re planning a solar install in the next several years, the 30% rate is stable and reliable. The urgency around “act now before the credit expires” that many installers use in their pitches is somewhat exaggerated for the near term — 2032 is nine years away. That said, there is no guarantee past 2034, so earlier is still better than later if the economics work for you.

What the 30% Applies To

This is where homeowners frequently underestimate the credit. The 30% applies to the full gross cost of the qualified installation, which includes more than just the panels:

Included in the credit calculation:

- Solar panels (modules)

- Inverters (string inverters, microinverters, power optimizers)

- Racking and mounting hardware

- Electrical wiring and conduit within the system

- Installation labor

- Permits and inspection fees

- Sales tax on all of the above

- Battery storage installed at the same time as the solar system (or in the same tax year)

- Monitoring equipment that is part of the solar installation

Not included:

- Roof repairs or replacement done at the same time as solar, unless the repair is directly required to support the solar installation (a gray area — consult a tax professional if your install included significant roofing work)

- EV charging equipment (that’s a separate credit — the Alternative Fuel Vehicle Refueling Property Credit, currently 30% up to $1,000 for residential)

- General electrical panel upgrades not directly related to the solar interconnection

My $28,210 system cost included panels, Enphase microinverters, racking, all labor, permit fees, and Austin city inspection fees. All of it was eligible. My installer provided an itemized invoice that I included with my tax records — useful if the IRS ever asks.

Battery storage note: I added my Tesla Powerwall in March 2023 — a separate installation from the November 2022 solar system. The Powerwall cost $11,500 installed. Because it was installed in a separate tax year and is a standalone battery (not co-installed with panels), I needed to confirm it qualified. Under IRS guidance, a home battery qualifies for the 30% Residential Clean Energy Credit if it has a capacity of at least 3 kWh and is charged exclusively (or primarily) by renewable energy. A Powerwall charged by rooftop solar qualifies. My additional credit for the Powerwall: $3,450, claimed on my 2023 tax return.

Total federal credits received across two years: $11,913 on $39,710 in total system costs. That is not a small number.

Who Qualifies

The credit is available to US homeowners who:

- Own their solar system — purchased outright (cash, solar loan, HELOC) or financed through a loan where you are the owner. Leased systems do not qualify. Systems under a power purchase agreement (PPA) do not qualify. The credit goes to the system owner, and if that’s a leasing company, you don’t get it.

- Install the system on a US residence — primary or secondary home. Investment properties and rental properties do not qualify for the residential credit (there is a separate commercial credit path for those).

- Have federal income tax liability — the credit is nonrefundable, meaning it can reduce your tax bill to zero but won’t generate a refund beyond that. If your federal tax liability for the year is $5,000 and your credit is $8,463, you get $5,000 of credit applied and the remaining $3,463 carries forward to the next tax year.

The carryforward provision is important: Unused credit doesn’t disappear. It carries forward to subsequent tax years until fully used. For most homeowners with reasonable incomes, the credit clears within one or two tax years. For retirees on fixed incomes with low tax liability, it may take several years to fully utilize. Plan accordingly — if you know your tax liability is low, discuss with a tax advisor whether to time your install to maximize utilization.

Who should think carefully before assuming they’ll use the full credit:

- Homeowners with low taxable income (retired, part-time employment, significant deductions)

- Homeowners who had an unusually high-income year they won’t repeat

- Homeowners who already carry other large credits (EV credit, child tax credit, etc.) that may exhaust their liability before the solar credit

For most working homeowners paying $8,000–$20,000+ in federal taxes annually, the credit is fully usable in the first year. For the 2022 install, I had more than enough tax liability to absorb the full $8,463 in one filing.

How to Actually Claim It

The credit is claimed on IRS Form 5695 (Residential Energy Credits), which you file with your federal income tax return (Form 1040) for the year the system was placed in service — meaning the year installation was completed and the system became operational, not the year you signed the contract or made a deposit.

If your system was installed in November 2024 and turned on in December 2024, you claim it on your 2024 return (filed by April 2025). If it was installed in December 2024 but didn’t pass final inspection and go live until January 2025, you claim it on your 2025 return.

What you need to file:

- Your installer’s final invoice showing the total system cost, itemized by component

- The date your system was placed in service (typically the date of final inspection or utility interconnection approval)

- IRS Form 5695 — Line 1 is where you enter the qualified solar electric property cost

The form is straightforward. Your tax software (TurboTax, H&R Block, FreeTaxUSA) will walk you through it with guided questions. If you use a CPA, tell them specifically that you installed solar in the tax year — it’s not always something they ask about proactively.

Keep documentation: Your installer invoice, any permits, interconnection agreement with your utility, and the date of final inspection. The IRS doesn’t require these documents at filing, but you’ll want them available if there’s ever a question.

The Credit and Your Financing Decision

The ITC interacts with your financing choice in a meaningful way that I covered in my financing comparison post — but it’s worth reiterating here.

If you financed with a solar loan, your loan was sized to cover the full system cost. The ITC credit comes back as reduced tax liability the following spring — it does not automatically pay down your loan. You need to take that tax credit savings and manually apply it as a lump-sum principal payment on your loan. If you don’t, you continue paying interest on the full pre-ITC loan balance for the entire term, which adds thousands of dollars in unnecessary interest over the life of the loan.

Most solar loans have a built-in “18-month balloon” or “step-up payment” structure specifically designed around the ITC: the loan assumes you’ll make a large principal payment equal to the ITC credit amount in year one, at which point the monthly payment is recalculated on the reduced balance. Read your loan documents carefully — if your loan has this structure, missing the balloon payment can trigger a rate increase.

Cash buyers don’t have this complexity. The credit comes back and goes into whatever account you choose. The way I think about the net cost of my system always uses the post-ITC number as the true baseline — $19,747 net, not the $28,210 gross.

2025 Update: Is the ITC at Risk?

This is a question I get versions of regularly, and it’s worth addressing directly.

The Inflation Reduction Act extended and codified the 30% rate through 2032. Repealing it before 2032 would require an act of Congress. As of 2025, there have been political discussions about modifying or accelerating phase-down of some IRA energy provisions — but the residential solar credit has broad bipartisan support at the district level because solar installation jobs exist in red and blue states alike. The political calculus for eliminating it is not straightforward.

That said: no tax provision is guaranteed permanently. If the economics of solar work for you today under the current 30% rate, waiting in hopes of the credit being extended or improved has limited upside. Waiting for it to potentially be reduced has meaningful downside. The people I know who delayed their solar decision by two to three years “waiting to see what happens” ended up installing at the same 30% rate they could have had earlier — just with two fewer years of electricity savings.

The credit is here, it’s 30%, and it’s stable through 2032. Use it.

— Allen